10 Ideas That I've Been Thinking About.

Welcome to my brain, I hope you enjoy.

Welcome to Young Money! If you’re new here, you can join the tens of thousands of subscribers receiving my essays each week by adding your email below.

Some ideas that I have been considering lately:

1) You should probably take more risks.

We live in a society that values margin of safety above everything. Because of this, we tend to delay "risky" activities to some point in the future. We tell ourselves that once we have more money or more experience, we will be in a better position to take a risk.

But that's not how risk works. Responsibilities increase with age, while time decreases.

The risky idea that could fail when you're 25? It won't ruin you. You have time to make that money back. But when you're 50 and putting your kids through school, you don't have that luxury. While it's uncomfortable to think about this in your 20s, you will get older. And your current opportunities won't be around forever.

Peak uncertainty when you are young is the best time to take that shot, because uncertainty = opportunity. If you fail? Who cares. You gain new stories and new friends. You have the rest of your life to make more money. And if it works? You won the game.

The risk of not taking any risks only grows exponentially with age. What are you going to do about it?

2) The importance of skin in the game.

In Skin in the Game, Nassim Taleb said, "Don’t tell me what you think, tell me what you have in your portfolio."

All investment advice could boil down to this one statement. We live in a golden age of grift, where selling is easier than building, and investment ideas are a dime a dozen. Be wary of those that provide investment "advice" without disclosing their own investments, or ask you to "invest" where they haven't.

Actions, not words, determine conviction. Skin in the game doesn't guarantee that the investment will pay off, but it does guarantee that all parties are subject to the same risks.

3) Short-term memories.

We tend to overweight the importance of current events, while we underweight evidence from the past. The Covid-19 pandemic may have been a once-in-a-lifetime experience for us, but historically it was hardly an outlier. In the history of the world's pandemics, it was actually quite mild. The Plague of Justinian killed half of Constantinople's population in four months. The Plague of 1771 killed one-third of Moscow's population in a single season.

Can you imagine four million New Yorkers dropping dead by September? That was the reality of prior pandemics. Covid-19 wasn't an outlier. It was mean-reversion.

Our memories of markets are even shorter. Financial bubbles are a staple of human behavior. From tulips to mortgages, no asset class is safe. The players and pieces change, but the plot remains the same. A story seduces investors one by one, and it spreads like wildfire. This story quickly outgrows any semblance of reality, but reality can stay suspended as long as the bubble continues to expand.

However, all of these stories end the same way: a massive inflow of money at peak valuations as investors are desperate to catch a hot trend, followed by a price decline as inflows slow, followed by a collapse as FOMO buyers become panic sellers.

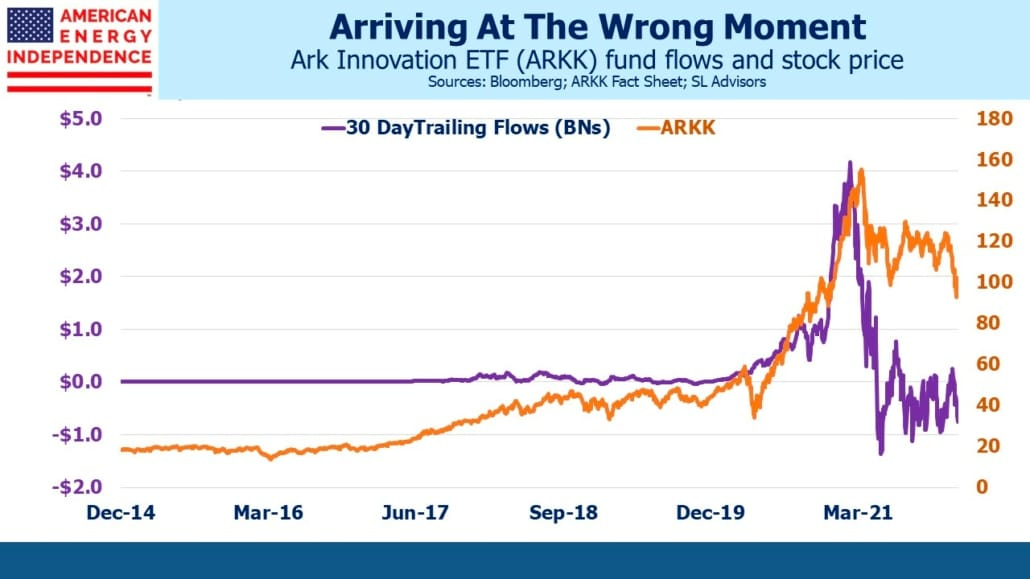

90% of Ark Invest's inflows came after their flagship ETF had gained 300% from its pandemic lows. Most of its holdings were trading at nosebleed valuations, but no price was too high for "disruptive innovation." It's no coincidence that these massive inflows marked the beginning of a 75% drawdown from ARKK's peak.

Similarly, crypto had higher inflows in the past year than any other time in history. And yet:

When the prices of our assets go up, we think we're geniuses. When prices of other people's assets go up, we want to join in on the fun. But sometimes prices go up just because people are buying stuff, not because that stuff is worth anything. And prices that go up for no reason can certainly drop for no reason.

Broken stories are rarely repaired, and stories without cash flows quickly fall from hero to zero when sentiment shifts.

Tulips, mortgages, growth stocks, cryptocurrencies. The assets are different, but the plot is the same. Too bad we don't study history. This time is different though, right?

4) There's no blueprint for how to do this.

Life is impossible to predict because so many random, uncontrolled variables come our way when we least expect them. Three years ago, I thought my career was set in stone. Work a few years, go to business school, and move my way up to a C-Suite job somewhere.

Now I write a blog and run some newsletters. Not exactly the typical finance/consulting route, but I'm not complaining. The point is, you don't have to follow some pre-ordained path. You certainly don't have to stay on a journey that you're not enjoying.

You don't have to work a specific job, live in a specific place, marry a specific person, or live any sort of specific life that you don't want to. You can quit, move, break up, or make changes whenever you want.

The idea of a correct way of doing things is the biggest obstacle preventing us from doing what we actually want. Worse still, we can get caught up in the monotonous routine of doing what we're supposed to do. Life isn't a spectator sport; it requires active participation. You aren't a passenger peering out the window of a 737. You are the pilot. Sure, you can cruise on autopilot. But picking your own destination is more interesting.

5) ESG isn't real.

ESG stands for "environmental, social, governance." A method for quantifying how good companies are. CNBC recently published its top 100 ESG companies. Number one? Alphabet, the parent of Google. The top seven include Microsoft, Bank of America, and Apple. Numbers 20 and 30 are Ford and GM. Number 58 is Northrop Grumman, an aerospace and defense manufacturer.

The four biggest holdings in Forbes' top-ranked ESG fund of May 2022, the Vanguard FTSE Social Index Fund (VFTAX), are *surprise* Apple, Microsoft, Amazon, and Alphabet. It does seem to me that "ESG" has been yet another label used to justify overweight big-tech positions for large funds, with no regard for neither E, nor S, nor G.

Interestingly, Tesla didn't make any ESG lists. You would think that the company that brought electric vehicles mainstream would get some "E" points, but I guess I just don't understand what ESG measures! I guess a defense manufacturer plays a much larger role in reducing our carbon footprint. To be fair, they do certainly help reduce the number of people.

6) The dollar has been a resilient inflation hedge.

There has been a lot of talk about inflation this year. How do we preserve our capital when the government is printing trillions of dollars? Apparently, we should have just hoarded those trillions of dollars.

Over the last 365 days, bitcoin is down 31%. The S&P is down 1%. The US dollar is up 15%.

Granted, this is in relation to other currencies, and domestic prices of goods have been increasing. But still, there is some irony that in this era of "money printing," the dollar has been one of the best-performing assets. Investing is hard.

7) You can't do by learning. You always learn by doing.

There's this idea that you need to hit a certain threshold of understanding before attempting a new task. You can't publish anything online until your writing improves. You can't converse in Spanish until you have memorized 1,000 words.

All of this studying feels productive, and sure, it can be useful to develop a knowledge base before diving headfirst into a new activity. But planning has diminishing returns. The best way to learn is by trying, failing, and iterating. Your language partner will correct your Spanish, and you will improve. Feedback (or lack-there-of) will help you find your writing voice. You can't do by learning. You always learn by doing.

Your likelihood of success is highly correlated to your tolerance for looking like an idiot in the short-term.

8) No one is going to save you.

We live in a unique era where survival is our base existence, not a state that we have to strive for. From nomadic tribes roaming the Asian Steppe to warring medieval European empires, 99% of societies throughout history had to actively work to stay alive. Apathy equaled death.

Today, in first-world countries, apathy is the status quo. Food, water, shelter? These are the norm, not the exception. Given that our base necessities are covered, we should be able to discover, build, and engage in amazing things. But there's a trillion-dollar industry that feeds off of our collective dopamine addiction, meaning that we can maintain the highest standard of living in history while spending 6 hours a day glued to our phones. How wild is that?

There is a proverb written by the English poet Violet Fane that says, "All things come to those who wait," which later became the now popular mantra: Good things come to those who wait. Unfortunately, this couldn't be further from the truth.

If you are living an exceptionally normal life with the expectation that one day, as a result of your exceptionally normal living, your life will become exceptionally extraordinary, I have a bridge to sell you.

You have a job? You went to school? Phenomenal work. So did everyone else. There isn't some grand prize for fulfilling our baseline societal expectations.

We believe that we are the protagonists of our own stories, and the universe will conspire to help us achieve our dreams if we just stay the course. But the universe doesn't give a damn about the aspirations of you, me, or anyone else. Good things don't come to those who wait. Good things come to those who create them.

Success isn't our default destination. Success is the result of disciplined, repeated action.

No one, not the universe, not God, not your company, not even your friends and family are going to save you. You aren't going to manifest your future by telling your peers that "your time is coming." You are just going to attract indifferent smiles from those who couldn't care less.

If you want something, it's on you to make it happen.

9) Look for asymmetrical returns.

When markets crash but the cash flows of underlying assets remain strong, you have an opportunity for outsized investment returns with minimal downside risk.

Direct messages and emails have zero downside and exponential upside.

Work that can be created once and distributed indefinitely creates asymmetrical input vs output.

When you discover situations that offer asymmetrical returns, situations where upside is exponential and downside is minimal, go all-in. These are the opportunities that can change your life.

10) Few things are more dangerous than early luck.

The luckier we get, the more confident we get. This is because luck is impossible to gauge, so we often mistake luck for skill. Misplaced luck creates disastrous outcomes.

Over the last couple of years, millions of new investors entered the market for the first time. Many generated insane returns. 10x. 20x. 30x. Life-changing money. And it was so easy. SPACs. Growth stocks. Crypto. It was all so easy. And when you make life-changing money, you're never going to dismiss it as "pure luck." You made the decision to buy those securities, after all.

However, market conditions over the last two years were anything but normal. It's not supposed to be this easy. But to new investors, this insanity was "normal." It was all they knew. Stories were driving valuations, and the fastest readers made the most money.

When your concentrated, risky bets turn massive profits, and you have never experienced a sentiment shift in a risk-off environment, obviously you are going to double down. Why wouldn't you? You 20x'd your money. You must know what you're doing.

The problem is, no one can fully appreciate risk until they experience it.

So you make another bet, and this one is 20x larger. But this time, the market isn't so favorable. Your "investment" gets cut in half. Instead of taking a step back and cutting your losses, you double down. You knew what you were doing the first time, after all. By the time you realize that your early gains may have been the byproduct of a friendly market instead of your skill, the money is gone.

That's why early luck is so dangerous. By getting lucky when you have little to lose, you get unlucky when you have everything to lose.

- Jack

I appreciate reader feedback, so if you enjoyed today’s piece, let me know with a like or comment at the bottom of this page!

Young Money is now an ad-free, reader-supported publication. This structure has created a better experience for both the reader and the writer, and it allows me to focus on producing good work instead of managing ad placements. In addition to helping support my newsletter, paid subscribers get access to additional content, including Q&As, book reviews, and more. If you’re a long-time reader who would like to further support Young Money, you can do so by clicking below. Thanks!